According to AXSMarine, commercial flows continued far below pre-conflict levels, with tanker, gas carrier and container traffic still operating under extreme uncertainty and elevated operational risk.

One month after the Strait of Hormuz ceased to function as an unobstructed passage for commercial shipping, April brought no clear normalization. Instead, vessel activity evolved through a sequence of short-lived recoveries, reversals, and renewed disruptions, shaped by ceasefire announcements, military enforcement actions, and continued security incidents.

Across dry bulk, tanker and gas carrier segments, traffic remained significantly below pre-conflict levels throughout the month. While brief windows of increased activity emerged, these proved fragile, with flows repeatedly resetting in response to geopolitical developments.

At the same time, AIS disruption, irregular vessel behaviour, and the growing presence of sanctioned or opaque operators continued to complicate visibility, making interpretation of underlying flows increasingly dependent on contextual analysis rather than raw tracking alone.

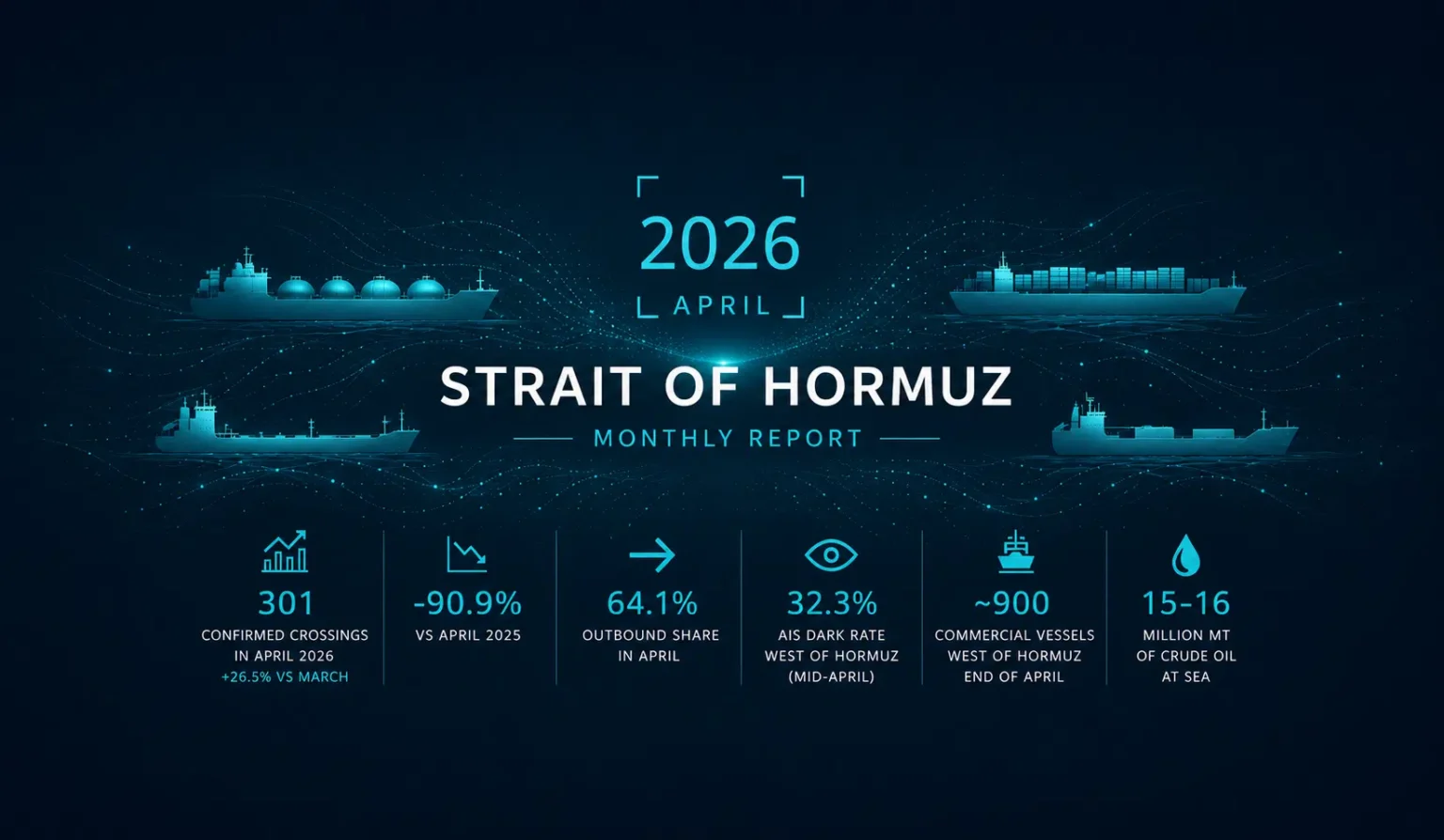

Across four tracked segments, confirmed April crossings rose to 301, up from 238 in March, representing a 26.5% month-on-month increase. However, this improvement came from an exceptionally low base. Compared with April 2025, when 3,297 crossings were recorded across the same broad group, activity remained down by 90.9%. Dry Bulk and MPP crossings were 83.9% lower year on year, tanker crossings were down 93.2%, gas carrier activity remained 87.9% below last year’s level, and liner traffic was still down 94.7%.

Outbound movements accounted for 64.1% of all April crossings, highlighting that operators were still prioritising exits from the Gulf over fresh inbound exposure.

Crossings: From Collapse to Fragmentation

Following the sharp contraction recorded in March, April opened with extremely limited activity. During the final week of March, confirmed crossings across dry bulk, tanker and gas carrier segments had averaged fewer than five per day. By early April, this figure began to recover gradually, reaching around ten daily crossings even before any formal ceasefire announcement.

The early-April US–Iran ceasefire introduced a temporary framework under which transit was expected to resume. This led to a measurable, but still modest, increase in activity. Between 1 and 7 April, 84 confirmed crossings were recorded, up from 48 during the preceding week.

The US Navy’s announced counter-blockade targeting Iranian ports and coastal movements reversed the upward trend almost immediately, pushing daily crossings back into single digits.

A second reopening window emerged on 17 to 18 April, following renewed political signals linked to a broader regional ceasefire. This produced the strongest activity of the entire post-disruption period, including 28 confirmed crossings on 18 April alone, with all major vessel segments participating.

The rebound proved short-lived. The reported seizure of the TOUSKA on 19 April, combined with further incidents and conflicting signals around the ceasefire, triggered an immediate collapse in traffic. In the three days that followed, crossings averaged just six per day, representing a sharp decline from the reopening window.

By the end of April, the Strait remained operational, but flows were fragmented. Vessel movements were no longer driven by commercial scheduling patterns, but by rapidly shifting security conditions, exemptions, and operator-specific risk tolerance.

Dry Bulk: Selective Activity, Outbound Bias

Dry bulk and multipurpose vessels accounted for a large share of the visible activity throughout April. Compared to other segments, these vessels appeared more willing to transit under uncertain conditions, particularly on outbound movements from the Gulf.

The overall pattern remained clearly imbalanced. Crossings were dominated by west-to-east movements, reflecting vessels exiting the region after discharge or repositioning, while inbound cargo flows remained more limited and selective.

Rather than indicating a recovery in trade flows, this activity points to a gradual clearing process, with operators prioritising exits over new exposure. Vessel behaviour, including AIS blackout usage and irregular signalling, also suggests that even within this segment, movements were highly conditional on risk tolerance.

Tankers: Risk Concentration and Selective Participation

Tanker activity remained heavily constrained and uneven throughout April.

A noticeable share of observed movements involved vessels linked to sanctioned, ghost fleet, or opaque ownership structures. These vessels were more frequently associated with AIS disruption, irregular routing, or non-standard operational patterns.

Conventional tanker participation remained limited. While both inbound and outbound movements were recorded, activity did not approach normal commercial levels and remained highly selective.

Large crude tanker movements continued to occur, but only intermittently. Isolated VLCC crossings were recorded later in the month, indicating that flows did not fully stop, but also did not return to any sustained or predictable pattern.

Inbound tanker traffic also continued on a selective basis, including crude carriers heading toward non-Iranian destinations, consistent with observed exemptions and routing behaviour during the period.

Gas Carriers: Persistent Sensitivity

Gas carriers remained one of the most constrained segments during April.

LPG vessels accounted for the majority of observed movements, with activity continuing at a reduced pace. A significant share of these vessels appeared linked to sanctioned or shadow fleet operators, indicating a concentration of activity among higher-risk participants.

LNG movements were particularly limited, with only two crossings recorded. This reflects both the operational sensitivity of LNG logistics and the lower tolerance for disruption across long-haul gas supply chains.

Overall, gas carrier activity remained highly dependent on risk conditions, with no indication of a broad-based recovery during the month.

Container Shipping: Security Risk Halts Market Return

The liner segment remained severely disrupted throughout April.

While a small number of container vessels continued to transit, activity was largely limited to Iranian, Iran-linked, or smaller regional operators. There was no visible return of major liner companies to the route.

Several incidents during the month reinforced the elevated risk environment. These included the attempted transit and subsequent seizure of EPAMINONDAS, as well as reported attacks involving vessels such as EUPHORIA and MSC FRANCESCA during or around transit operations.

Such events highlight the structural challenges facing liner shipping in the region. Unlike other segments, container shipping depends on schedule reliability and stable network planning, both of which remained unachievable under April conditions.

Fleet Congestion and Positioning

At the height of the disruption, more than 1,000 merchant vessels had accumulated west of Hormuz inside the Gulf.

By early April, total tracked vessels across both sides of the Strait stood at around 1,441, with 959 positioned inside the Gulf. While this represented some easing from peak congestion levels, the backlog remained substantial.

Over the course of the month, this congestion gradually declined. By the end of April, the number of commercial vessels west of Hormuz had fallen to approximately 900.

This reduction does not indicate normalization. Rather, it reflects a combination of selective departures, constrained inbound flows, and continued hesitation among operators to commit tonnage under uncertain conditions.

AIS Disruption and Market Visibility

AIS disruption remained central to understanding the April operating environment.

Vessels continued to operate under extended blackout conditions, reappear after prolonged signal gaps, or transmit irregular and sometimes misleading destination and cargo information. In several cases, transponders were reactivated only after a transit had been completed or aborted, limiting the ability to verify movements in real time.

As of mid-April, 949 vessels were still tracked west of Hormuz, with 307 operating under blackout conditions. This placed the regional AIS-dark rate at around 32 percent, more than double the pre-conflict baseline of approximately 17 percent.

By month-end, although total vessel counts inside the Gulf had declined to around 900, visibility remained impaired.

The impact of AIS disruption was particularly pronounced among tankers, dry bulk vessels, and ships linked to sanctioned or opaque ownership structures. These segments showed a higher incidence of signal suppression, manipulation, or irregular reporting behaviour.

As a result, confirmed visible crossings represent only part of the picture. Interpreting actual activity requires combining AIS data with vessel identity, ownership patterns, cargo indicators, and behavioural context.

Oil at Sea: A Backlog Waiting for Resolution

As of late April, an estimated 15 to 16 million metric tons of crude oil remained stored aboard vessels within the Gulf.

Using a standard conversion factor for Middle Eastern crude grades, this corresponds to approximately 108 to 117 million barrels of oil at sea.

At pre-conflict transit rates of 15 to 20 million barrels per day through the Strait of Hormuz, this volume could theoretically clear within six to eight days following a full reopening.

In practice, however, delivery timelines would extend significantly. Typical voyage durations imply around two weeks to southern China and up to three weeks to northern Asia.

At the same time, any reopening would likely coincide with a resumption of terminal activity, introducing new loading volumes alongside the existing backlog. As a result, flows would be expected to scale gradually rather than normalize immediately.

Conclusion: A Corridor Constrained in Practice

April demonstrated that reopening the Strait of Hormuz is not a binary event.

Traffic responded quickly to ceasefire signals, but just as quickly reversed under renewed military pressure, vessel attacks, and enforcement actions such as the US counter-blockade.

Rather than a steady recovery, the market experienced a fragmented operating environment in which access depended on timing, vessel profile, ownership structure, and risk tolerance.

Even as congestion eased toward around 900 vessels west of Hormuz by month-end, flows remained far below normal levels.

The Strait continued to function not as a fully open global trade artery, but as a constrained and selectively accessible corridor shaped by geopolitical risk.